Intro

This finding reshapes how crypto-native prediction market infrastructure should be designed, funded, and valued. The precise share fluctuates seasonally: during NFL peak months (September-February), sports exceed 75–80% of combined volume across Kalshi and Polymarket; during major election cycles, it dips below 60% before snapping back.[1]

The $44 billion prediction market industry in 2025 [2] is, at its core, a sports betting industry wearing prediction market clothing - and understanding why reveals deep truths about liquidity formation, behavioral economics, and protocol design.[3]

The data behind the ~70% claim

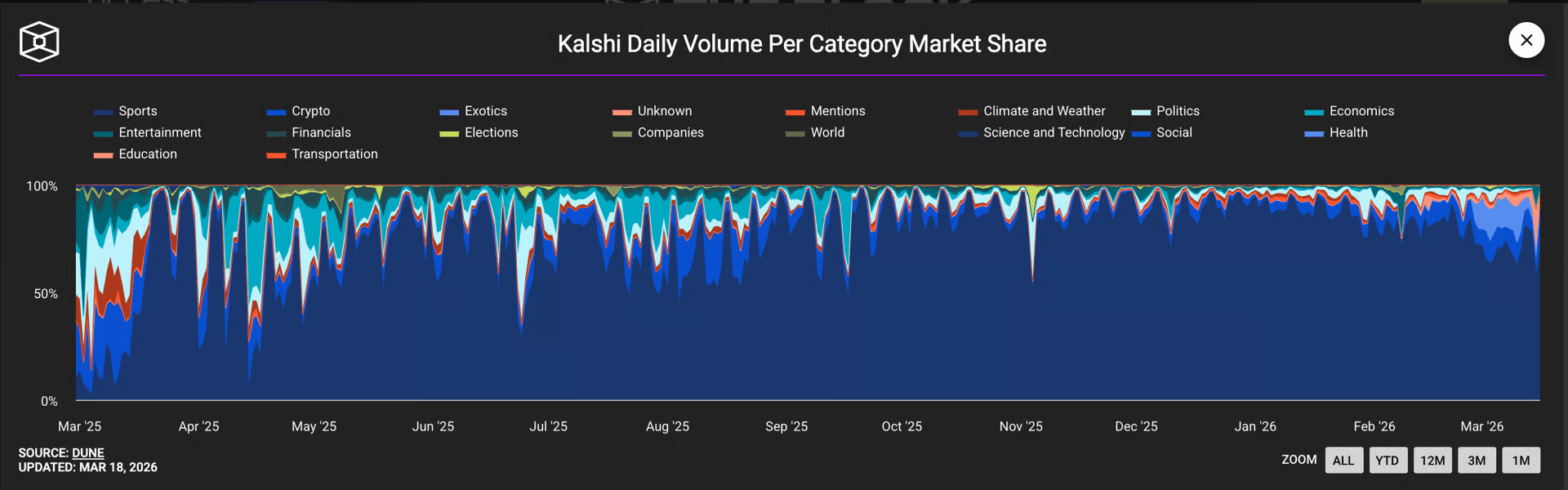

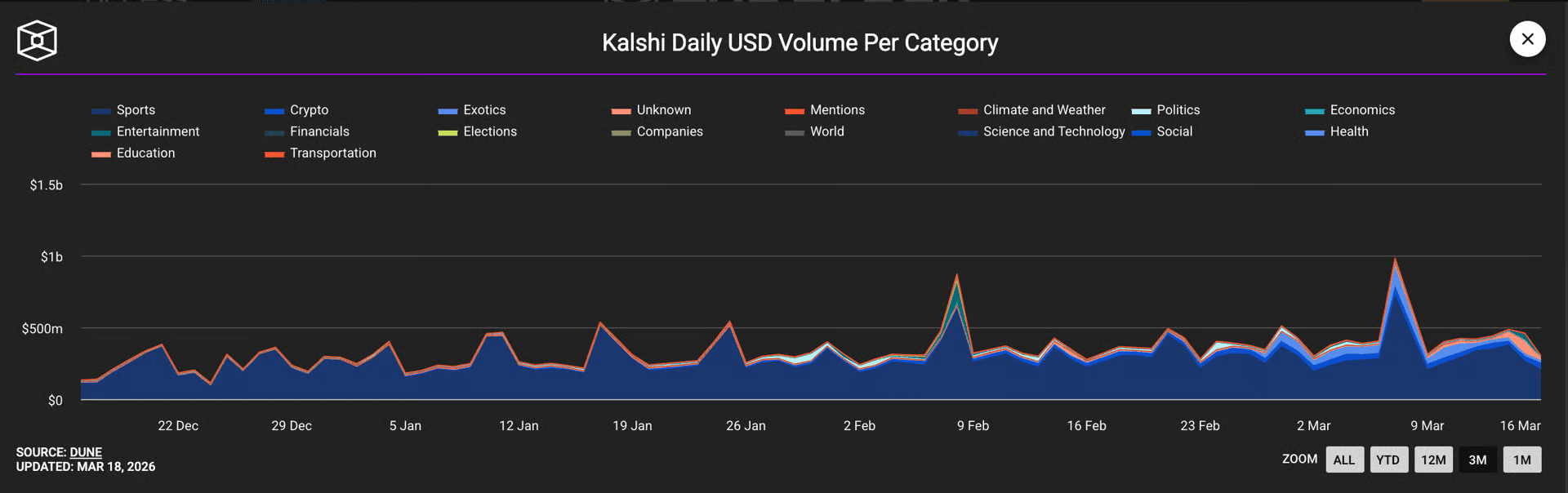

The claim that sports represent approximately 70% of prediction market volume holds up under weighted analysis, though the number requires platform-level decomposition. Kalshi, which processed $22.88 billion in 2025 volume [4], derives 85–90% from sports (~$19.4B).

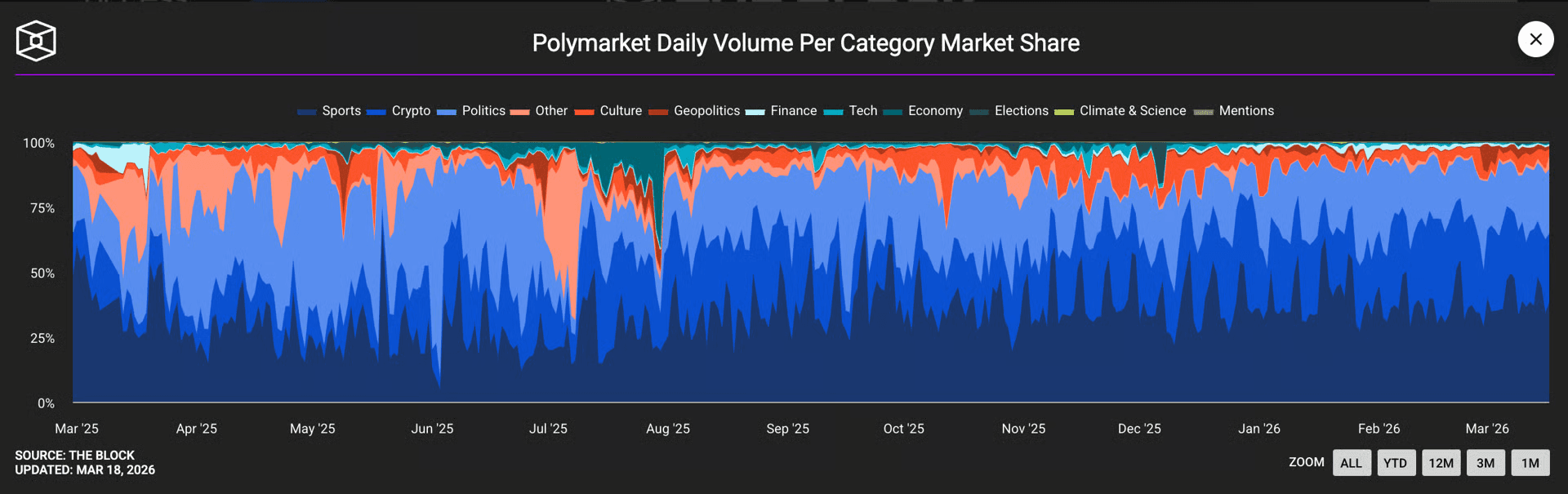

Polymarket, with $21.5 billion in 2025 volume, is more diversified [5]: sports account for 39% (~$8.4B), politics 34%, and crypto 18%. Combining just these two platforms - which together represent 85–90% of global prediction market activity - yields a sports share of approximately 62.7%.

Adding sports-focused protocols like Azuro ($390M+ lifetime) and SX Bet ($460M+ lifetime) along with estimated sports share from smaller platforms, pushes the aggregate to 66–70%. The seasonal dynamics are striking. During Kalshi's NFL-dominated months (September–December 2025), sports exceeded 90% of platform volume, generating $138 million in sports fee revenue alone.[6] Polymarket's post-election pivot saw sports emerge as "the most popular sector" after political volume crashed 84% overnight following the November 2024 US election [7].

Weekly data from February 2026 confirms the pattern: Kalshi sports volume of $2.21 billion (85.4% of platform) plus Polymarket sports of $721 million (39.6%) yields a combined sports share of 66.4% - rising toward 70% when smaller all-sports platforms are included.

A critical caveat emerges from the volume-versus-capital distinction. Sports dominate volume but not open interest. On Kalshi, politics, elections, and economics combined hold 2.5× the open interest of sports. On Polymarket, politics outpaced sports by 400% in open interest during 2025. This reveals sports' true structural role: it functions as the market's flow engine (high turnover, frequent small trades) while non-sports categories serve as the capital engine (fewer but larger positions held longer).

Mass-market platforms including DraftKings, FanDuel, and Robinhood rolled out regulated prediction products ahead of the 2026 FIFA World Cup, set to be hosted in North America [8].

Eilers and Krejcik project sports will settle at ~44% of long-run volume as other categories mature [9], suggesting current dominance partially reflects the nascency of non-sports prediction markets rather than a permanent structural equilibrium.

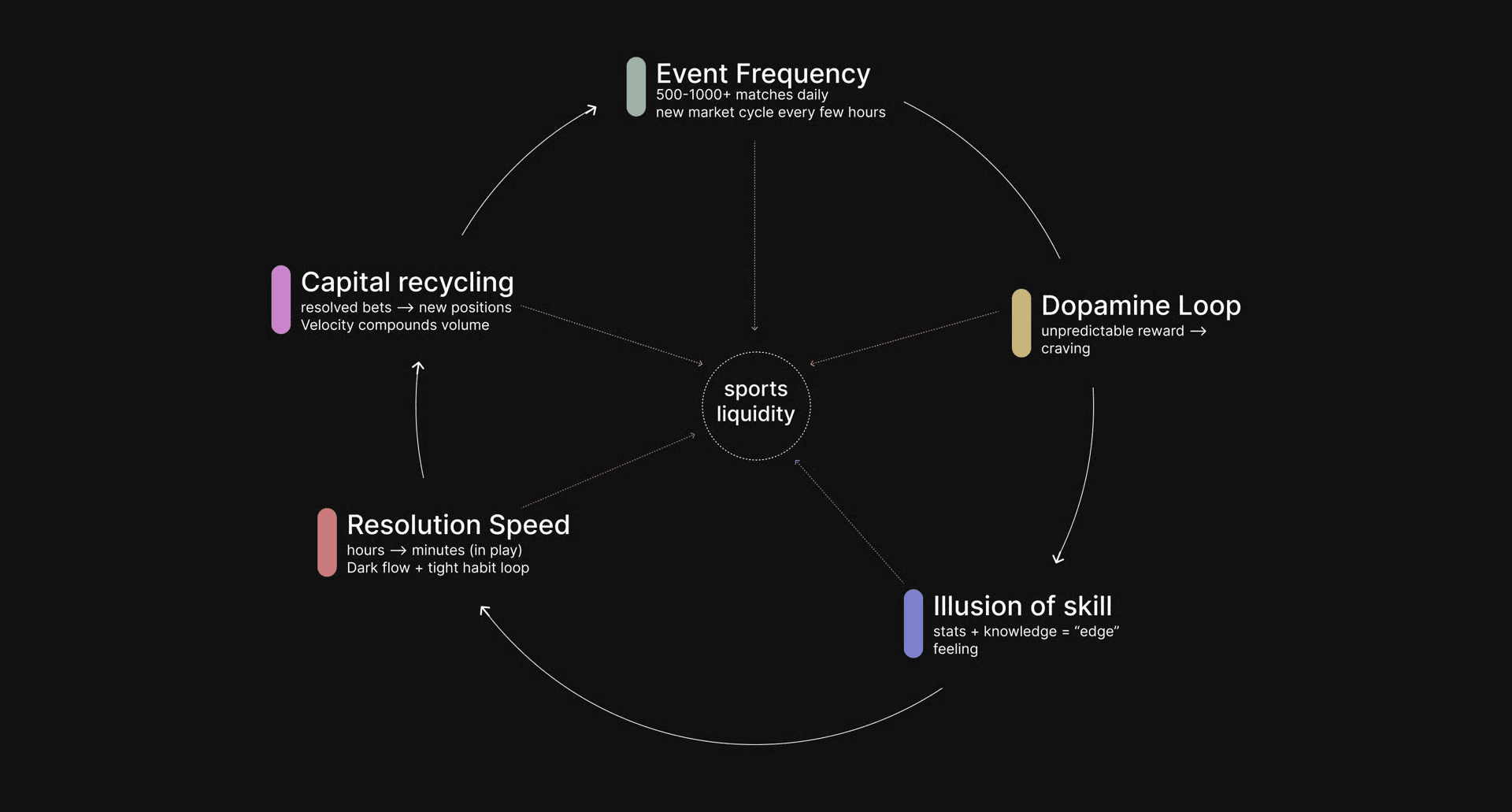

The behavioral flywheel that makes sports unbeatable

Sports' dominance stems from a five-part behavioral flywheel that generates compounding engagement advantages no other prediction market category can match.

Event frequency is the foundational driver. Soccer alone produces 500–1,000+ bettable matches daily worldwide, generating over $800 billion in betting turnover in 2025 [10]. The NFL offers 267 games per season, the NBA 1,230, and MLB 2,430 — and these represent only American leagues. Political prediction markets, by contrast, produce meaningful events perhaps dozens of times per year. This frequency gap is not incremental; it is orders of magnitude. High event frequency directly creates liquidity because each event represents a new market cycle: creation → price discovery → trading → resolution → capital recycling. Sports markets complete this cycle in hours, while political markets take weeks to months. The capital velocity difference alone explains much of the volume gap.

Neurochemical reward loops exploit this frequency ruthlessly. Dopamine release during gambling reflects the unpredictability of reward delivery rather than the reward itself, according to research published in the Journal of Neuroscience [11]. Sports outcomes involve genuine uncertainty within compressed timeframes, creating tight bet-outcome-reward loops that maximize dopamine conditioning. The near-miss phenomenon is particularly potent in sports: missing a parlay by one game activates the same reward circuits as actual wins, creating the illusion that success is imminent.

The illusion of skill creates uniquely persistent engagement. Unlike casino games or even political prediction markets, sports bettors genuinely believe their knowledge - of teams, players, statistics, matchups - provides a meaningful edge. This "overconfidence bias" is, according to NYU Stern research [12], "perhaps the most prevalent bias in sports betting." A Stanford field experiment found pervasive overoptimism about financial returns among sports bettors more so than lottery players. This illusion sustains engagement far longer than markets where randomness is obvious. In prediction market terms, sports create what behavioral economists call "skilled gambling" perception: users feel they are making informed analytical decisions rather than placing bets, which reduces psychological friction around losses and increases willingness to re-engage.

Resolution speed completes the loop. Sports markets resolve in hours or minutes (with in-play micro-betting), creating the tight temporal coupling between action and outcome that behavioral research identifies as essential for habit formation. The concept of "dark flow" a trance-like, dissociative state originally documented in slot machine play [13] has been extended to sports betting apps by Kindbridge Behavioral Health, noting that modern apps create "a seamless experience for users, allowing them to transition from one movement to the next." Political prediction markets, with resolution cycles measured in months, simply cannot induce these states.

Market microstructure reveals sports' structural advantages

A landmark 2026 analysis by Becker examining 72.1 million trades and $18.26 billion in volume on Kalshi found that sports account for 72% of notional volume despite having moderate efficiency (maker-taker gap of 2.23 percentage points versus 0.17 pp for finance markets) [14]. This inefficiency is not a weakness but a feature: it means sports markets transfer the most wealth from retail takers to sophisticated makers, creating powerful economic incentives for market makers to provide liquidity specifically in sports. Finance markets approach perfect efficiency but generate negligible absolute returns for liquidity providers. Sports markets are the Goldilocks category - inefficient enough to be profitable for market makers, efficient enough to attract massive retail volume.

The maker-taker dynamics evolved dramatically over time. In Kalshi's early days (2021–2023), takers earned +2.0% while makers lost -2.0%. After professional liquidity providers entered post-2024, the relationship inverted: makers now earn +2.5 pp while takers lose equivalently. This 5.3 percentage point swing represents the professionalization of prediction market liquidity provision. Palumbo's 2026 SSRN analysis of NFL contract liquidity found that market making in event-contract markets resembles underwriting more than traditional market making - profitability depends on managing terminal risk (exposure at settlement) rather than capturing bid-ask spreads [15]. This structural insight explains why institutional firms like Jump Trading have entered prediction market liquidity provision.

Price discovery patterns further illuminate sports' advantages. Research by Ng, Peng, Tao & Zhou (January 2026) provides the first rigorous evidence that Polymarket leads Kalshi in price discovery when liquidity is high, with net order imbalance from large trades strongly predicting subsequent returns. Significant price disparities persist across platforms, implying economically meaningful arbitrage opportunities which in turn attract algorithmic traders who provide additional liquidity. Cross-platform arbitrage between Polymarket and Kalshi on identical sports events has become a cottage industry: a Polymarket YES at $0.45 against a Kalshi NO at $0.52 yields a risk-free 3% return, with windows lasting seconds and captured primarily by bots.

Rigorous empirical analysis of prediction market microstructure confirms sports' dominance is not merely behavioral - it is deeply embedded in how these markets function at the order-flow level.

Conclusion: sports as the liquidity primitive

The dominance of sports in prediction markets is not a transient artifact of market nascency - it reflects deep structural advantages across every dimension that matters for market formation. Neurochemically, sports create tighter dopamine loops than any competing category. Temporally, thousands of daily events with hour-scale resolution cycles generate capital velocity that political markets (monthly resolution) and crypto markets (variable resolution) cannot approach. Microstructurally, sports markets occupy the optimal efficiency zone — inefficient enough to compensate market makers generously (2.23 pp maker-taker gap) while efficient enough to attract massive retail flow.

Three forward-looking insights emerge for crypto fund positioning:

First, sports are the liquidity primitive for prediction markets — the base layer of engagement and capital velocity upon which all other categories depend. Platforms that fail to capture sports volume will struggle to sustain the user base needed for non-sports markets.

Second, the volume-versus-open-interest divergence reveals that sports and non-sports markets serve complementary economic functions. The most valuable prediction market platforms will be those that use sports as the retention engine while monetizing higher-margin, longer-duration political and economic markets for capital deployment.

Third, Paradigm's pm-AMM research suggests that AMM-based prediction markets remain theoretically promising but practically unproven - the CLOB model (Polymarket, Kalshi, SX Bet) has won the current generation, but Azuro's singleton pool approach may prove superior for the specific high-frequency, multi-market characteristics of sports betting.

The prediction market sector's $3.71 billion in 2025 fundraising [26] and combined $20B+ valuations for Polymarket and Kalshi are, fundamentally, bets that sports-driven liquidity can be the foundation for a new financial asset class worth hundreds of billions.

Building something interesting? We back founders shipping the next generation of crypto infrastructure.

Work with us →gMJ: The holy grail of sports cards is on-chain and underpriced

The most iconic trading card ever printed now trades like a token 24 hours a day on Uniswap — and it sits at a 5–7% discount to its real-world price.

gSPEED: the first memecoin with a floor under it

Every SPEED token before this one is now worth a rounding error. gSPEED is different — each token is a fractional claim on a real, vaulted iShowSpeed PSA 10. A meme with a redemption floor.